Introduction

The SEC Marketing Rule governs many marketing communications used by SEC-registered investment advisers and advisers required to register with the SEC, including communications that appear on websites, in decks, and across social media.

For hedge funds and private fund advisers, this matters because the website is no longer just a credibility asset. It can also be an advertisement under Rule 206(4)-1.

This article explains what the rule restricts, where firms keep getting caught, and how advisers can build credibility online without creating unnecessary regulatory exposure.

This article is for general information only and is not legal advice. Marketing Rule compliance is fact-specific. Confirm any decision with your CCO or outside counsel before publishing.

Most Advisers Treat Marketing as a Compliance Afterthought. The SEC Treats It as a Fraud Risk.

For hedge funds and private fund advisers, the instinct around marketing has always been caution.

Say less. Avoid anything that looks promotional. Let the track record speak in the room and keep the website thin.

That instinct is now a liability for a different reason than most firms assume.

The problem is no longer only that a thin website makes a strong firm look invisible. It is that the website itself may be a regulated advertisement, and the regulator has been actively fining advisers for what appears on public-facing marketing materials.

Since the Marketing Rule’s compliance date, the SEC has brought enforcement actions targeting website content specifically: hypothetical performance, unsubstantiated claims, improperly disclosed testimonials, endorsements, and third-party ratings.

The firms charged were not all running aggressive retail campaigns. Several issues involved public website language, performance figures, ratings, testimonials, or claims that lacked the supporting structure required by the rule.

If you are an SEC-registered adviser, your marketing sits inside a specific legal framework.

Understanding that framework is not a constraint on building visibility. It is the precondition for building it without creating unnecessary regulatory exposure.

What the Marketing Rule Is

Rule 206(4)-1 under the Investment Advisers Act of 1940 is the rule the industry calls the Marketing Rule.

The SEC adopted the modernized rule in December 2020. It became effective on May 4, 2021, with a mandatory compliance date of November 4, 2022.

It consolidated and replaced the old advertising rule and the separate cash solicitation rule into a single marketing framework.

The rule applies to investment advisers registered or required to be registered with the SEC. That includes advisers to private funds.

If you are an SEC-registered hedge fund adviser, you are inside its scope.

The rule text is the baseline. What continues to develop is the interpretive and examination layer around it. The SEC’s Division of Investment Management maintains Marketing Compliance FAQs, and the Division of Examinations has issued risk alerts showing where examiners are looking.

Those FAQs and risk alerts are staff views, not rule text. But for advisers trying to understand regulatory attention, they are still important signals.

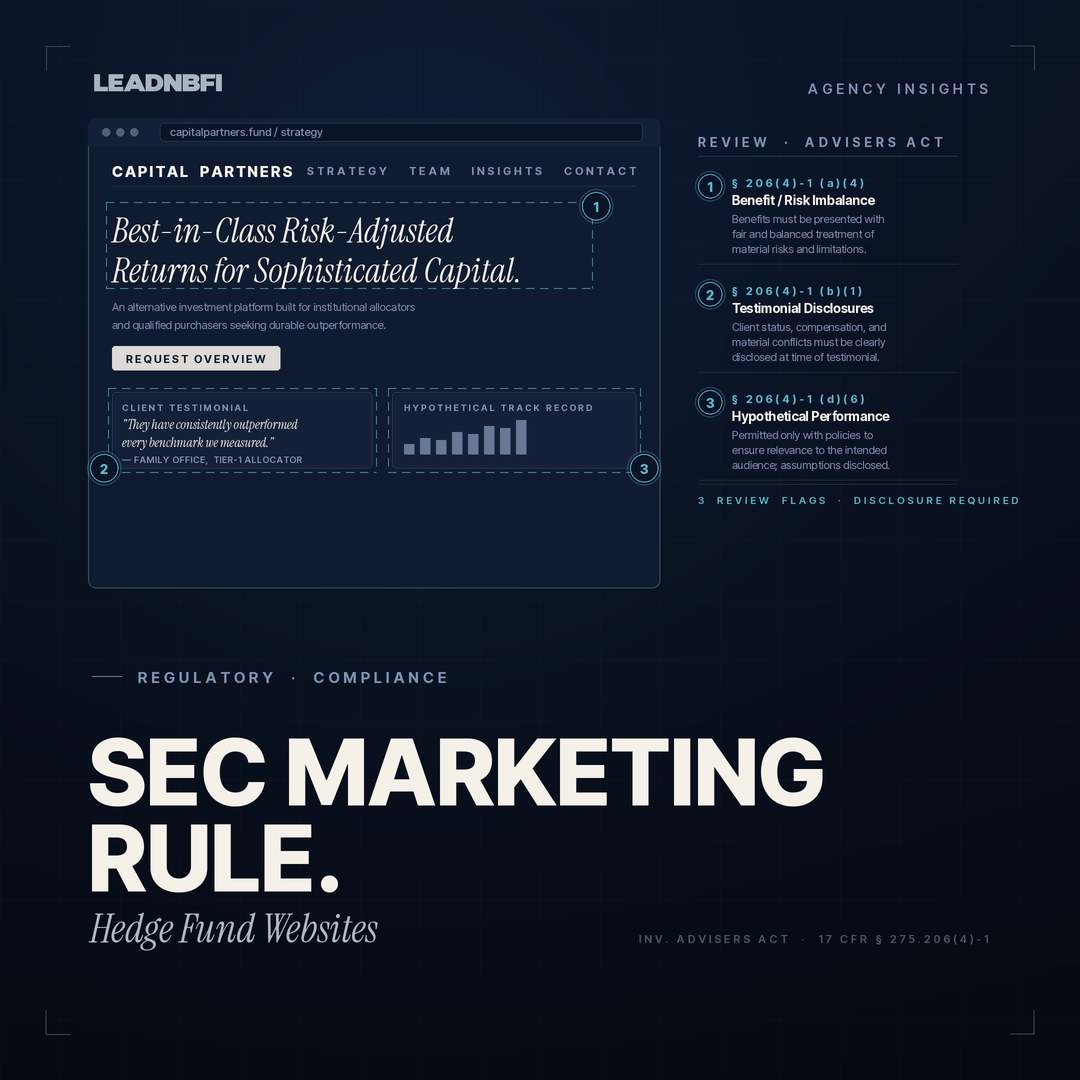

Your Website Can Be an Advertisement

The single most important thing to understand is the scope of the word “advertisement.”

It is broader than the brochure-era definition many advisers still carry in their heads.

The rule defines an advertisement in two parts.

The first covers certain direct or indirect communications an adviser makes that offer its advisory services to prospective clients or private fund investors, or offer new services to existing clients or investors.

The second covers testimonials or endorsements for which the adviser provides compensation, directly or indirectly.

In practice, that means the following can fall within the rule when they promote advisory services, performance, ratings, testimonials, or endorsements:

- Public websites and microsites

- Firm and personnel pages on LinkedIn and other platforms

- Email campaigns and digital newsletters sent to more than one recipient

- Pre-scripted or reused videos, webcasts, and podcasts

- Content created by anyone compensated to promote the adviser, including referral partners and paid promoters

There is no separate, lighter rulebook for digital content.

The SEC applies the same principles-based framework to a website that it applies to a printed pitchbook, and its risk alerts make clear that websites and social media are examination priorities, not side issues.

For hedge fund advisers, this is why website copy, performance language, awards, ratings, testimonials, and even broad credibility claims need to be reviewed carefully before publication.

The Seven General Prohibitions

The backbone of the rule is a set of seven general prohibitions that apply to advertisements.

An advertisement may not:

- Include an untrue statement of material fact, or omit a fact needed to keep a statement from being misleading.

- Include a material statement of fact the adviser does not have a reasonable basis to believe it can substantiate on demand by the SEC.

- Include information likely to cause a false or misleading implication about a material fact.

- Discuss potential benefits without fair and balanced treatment of associated material risks or limitations.

- Reference specific investment advice in a manner that is not fair and balanced.

- Include or exclude performance results, or present time periods, in a manner that is not fair and balanced.

- Otherwise be materially misleading.

Two of these deserve special attention because they catch many firms.

The substantiation requirement means that for any material factual claim on your site, you need a reasonable basis to believe you can prove it if the SEC asks.

If you cannot produce support on demand, the SEC may presume you did not have a reasonable basis.

This is what turns a vague marketing phrase into a compliance problem.

A claim that your firm is “free of conflicts of interest,” “institutionally validated,” “best in class,” or “award-winning” is not just stylistic language. It may be treated as a factual assertion you may be asked to document.

The fair-and-balanced requirements mean that benefits cannot appear without corresponding risks or limitations, and that performance cannot be presented selectively.

Cherry-picking strong outcomes is not a gray area. It is exactly the kind of presentation the rule is designed to prevent.

Performance Is the Highest-Risk Content You Can Publish

Performance advertising carries the most detailed conditions in the rule and has produced repeated enforcement actions.

The provisions that matter most for a hedge fund or private fund adviser website are straightforward.

Gross Performance Requires Net Performance

You may not show gross performance in an advertisement unless you also show net performance with at least equal prominence, in a comparable format, over the same time period, using the same type of return and methodology.

A gross figure standing alone is a problem.

Standardized Time Periods

For portfolios other than private funds, performance must generally be shown over one-, five-, and ten-year periods, each with equal prominence, ending no earlier than the most recent calendar year-end.

Private fund performance is exempt from that prescribed one-, five-, and ten-year format, but it must still be fair and balanced.

Extracted Performance

If you pull the performance of a subset of investments out of a portfolio, you generally need to show, or offer to promptly provide, the performance of the total portfolio as well.

SEC staff has issued a narrow no-action position permitting gross-only extracts under specific conditions, but the default rule still requires advisers to avoid presenting a partial picture in a misleading way.

Hypothetical Performance Is the Trap

Hypothetical performance includes model performance, backtested results, and targeted or projected returns.

The rule permits hypothetical performance only if the adviser adopts and implements policies and procedures reasonably designed to ensure that the hypothetical performance is relevant to the likely financial situation and investment objectives of the intended audience.

The adviser must also provide sufficient information about the criteria, assumptions, risks, and limitations.

That is difficult to do on a public website, because the audience is unknown and unlimited.

The SEC’s adopting release states that advisers generally would not be able to include hypothetical performance in advertisements directed to a mass audience or intended for general circulation, because the adviser generally could not form expectations about the audience’s financial situation or investment objectives.

In practical terms, putting backtested, model, targeted, or projected returns on a public hedge fund website is a high-risk practice and difficult to defend unless the firm has a very specific, counsel-reviewed structure supporting it.

What the SEC Has Actually Fined Firms For

The enforcement record is the clearest guide to where the lines are.

Titan Global Capital Management

Titan Global Capital Management was the first Marketing Rule enforcement action.

The SEC found that Titan advertised hypothetical performance metrics without adopting and implementing required policies and procedures or taking other required steps under the Marketing Rule.

Titan agreed to pay $192,454 in disgorgement and prejudgment interest and an $850,000 civil penalty.

The September 2023 Sweep

In September 2023, the SEC charged nine registered investment advisers for advertising hypothetical performance to the general public on their websites without adopting or implementing the policies and procedures required by the Marketing Rule.

The firms agreed to pay $850,000 in combined penalties.

Two advisers also failed to maintain required copies of their advertisements.

The April 2024 Sweep

In April 2024, the SEC charged five more registered investment advisers for Marketing Rule violations.

The core issue was again hypothetical performance advertised to the general public on websites without policies and procedures reasonably designed to ensure the hypothetical performance was relevant to the likely financial situation and investment objectives of the intended audience.

The firms agreed to pay $200,000 in combined penalties.

One firm, GeaSphere, was also cited for additional issues, including false and misleading statements in advertisements, misleading model performance, inability to substantiate performance shown in advertisements, and failure to enter into written agreements with compensated endorsers.

The September 2024 Sweep

In September 2024, the SEC charged nine registered investment advisers for violating the Marketing Rule by disseminating advertisements that included untrue or unsubstantiated statements of material fact, or testimonials, endorsements, or third-party ratings that lacked required disclosures.

The firms agreed to pay $1.24 million in combined civil penalties.

The SEC’s orders included issues involving untrue statements about third-party ratings, claims of conflict-free advisory services that firms could not substantiate, testimonials that did not come from current clients, paid endorsements without required disclosures, and third-party ratings that lacked date or period disclosures.

The pattern is consistent.

The conduct that gets fined is often public-facing, often website-based, and often involves performance, unsubstantiated credibility claims, testimonials, endorsements, ratings, or missing policies.

For financial firms trying to build authority online, this is the core lesson: the issue is not marketing itself. The issue is marketing that cannot be substantiated, balanced, disclosed, or archived.

Testimonials, Endorsements, and Ratings Are Allowed, but Heavily Conditioned

The Marketing Rule reversed the old near-total ban on testimonials.

Client testimonials, compensated endorsements, and third-party ratings can now be used, but only inside a strict set of conditions.

For testimonials and endorsements, the advertisement must clearly and prominently disclose whether the promoter is a client, whether they are compensated, and the material terms of any compensation and conflicts.

Advisers generally need a written agreement with compensated promoters, unless an exception applies, such as certain affiliate relationships or de minimis compensation.

De minimis compensation means $1,000 or less, or its non-cash equivalent, over a twelve-month period.

Advisers also cannot compensate an ineligible person who is subject to certain disqualifying events.

For third-party ratings, the adviser must have a reasonable basis to believe the questionnaire or survey used to prepare the rating was not designed to produce a predetermined result.

The advertisement must also clearly and prominently disclose the date of the rating, the period it covers, and whether compensation was provided in connection with obtaining or using the rating.

The recurring failure is disclosure placement.

Required disclosures need to be clear and prominent. They should not be buried on a separate disclosures page, hidden behind a link, or placed far away from the claim they qualify.

A testimonial, endorsement, rating, or award on your website should be reviewed as part of the advertisement itself, not as a design element added after the fact.

How Compliant Firms Build Credibility Within the Rule

None of this means a fund website has to be a thin, defensive brochure.

It means credibility has to be built from materials that survive substantiation rather than from claims that invite regulatory pressure.

The strongest compliant hedge fund and adviser sites usually do the following.

They Lead With Specificity Instead of Superlatives

“We focus on lower-middle-market industrials” is a verifiable positioning statement.

“We are a best-in-class manager” is an unsubstantiated claim unless the firm can clearly support it.

Specificity is both better marketing and safer compliance.

It gives allocators, consultants, founders, and counterparties a clearer understanding of what the firm actually does without relying on vague superiority language.

This is especially important for hedge fund marketing, where credibility depends on precision, restraint, and evidence.

For more on hedge fund positioning, see LeadNBFI’s hedge fund marketing page.

They Build Authority Through Thinking, Not Unsupported Numbers

Market commentary, investment perspective, and demonstrated judgment can establish credibility without triggering the same performance-advertising risks as public return claims.

This is where content can do the work that a public performance table often cannot.

For many hedge funds and private fund advisers, the better public website strategy is not to show more numbers. It is to show clearer thinking, sharper positioning, and a more credible explanation of the firm’s strategy, process, and market view.

That is the role of content marketing for financial services.

They Treat Performance as a Compliance Project, Not a Design Asset

If performance appears on a website, it should not be treated as a graphic design element.

It needs net alongside gross where required, proper time periods, consistent methodology, fair and balanced presentation, and the disclosures needed to avoid misleading the audience.

Hypothetical, backtested, model, targeted, or projected performance should generally stay off public pages unless counsel and compliance have specifically reviewed the structure.

They Archive the Website Like a Regulated Record

The amended books-and-records rule requires advisers to keep copies of advertisements and documentation supporting material claims.

That means website updates, landing pages, social posts, video scripts, email campaigns, testimonials, endorsements, ratings, and performance materials need to be retained.

The firms that pass exams have an archiving process, not just a publishing workflow.

They Design Disclosures Into the Layout From the Start

Disclosures should not be treated as a footer problem.

If a performance figure, testimonial, endorsement, rating, or award needs disclosure, the disclosure should be designed into the page near the relevant claim.

This is both a compliance issue and a trust issue.

Sophisticated financial buyers notice when a firm communicates precisely. They also notice when claims look inflated, vague, or unsupported.

That is why corporate branding for financial firms should be built with compliance review in mind from the start.

The Marketing Rule Does Not Make Good Marketing Impossible

The Marketing Rule and good financial services marketing point in the same direction.

Both reward precise positioning, demonstrated expertise, balanced presentation, and verifiable claims.

The firms that get into trouble are usually reaching for shortcuts the rule was written to stop: exaggerated performance, unsupported superiority claims, undisclosed paid endorsements, stale ratings, and copy that says more than the firm can prove.

The firms that build durable visibility take the opposite path.

They make their credibility legible and provable.

That is what a sophisticated allocator, founder, business owner, sponsor, or counterparty is looking for anyway.

Frequently Asked Questions

Does the SEC Marketing Rule apply to hedge funds and private fund advisers?

Yes. Rule 206(4)-1 applies to investment advisers registered or required to be registered with the SEC, and the rule includes advisers to private funds.

If your hedge fund adviser is SEC-registered, its website, decks, social media, and other marketing communications may be subject to the rule when they fall within the definition of advertisement.

Is a hedge fund website considered advertising under the rule?

It can be.

The rule’s definition of “advertisement” covers certain direct or indirect communications that offer advisory services to prospective clients or private fund investors, or offer new services to existing clients or investors.

Public websites, microsites, and social-media content can fall within that definition when they promote advisory services, performance, testimonials, endorsements, or ratings.

Can an investment adviser show performance on its public website?

It can, but with strict conditions.

Gross performance generally must appear alongside net performance with equal prominence, over the same period, using the same type of return and methodology.

Non-private-fund performance generally must use standardized one-, five-, and ten-year periods.

Private fund performance is not subject to that prescribed one-, five-, and ten-year format, but it must still be fair and balanced.

Hypothetical, backtested, model, targeted, or projected performance on a public website is especially high-risk because the audience is unknown.

Why is hypothetical performance such a high-risk practice?

Because the rule only permits hypothetical performance when the adviser has policies and procedures reasonably designed to ensure the hypothetical performance is relevant to the likely financial situation and investment objectives of the intended audience.

On a public website, the audience is broad and unknown, making that condition difficult to satisfy.

The SEC has brought multiple enforcement sweeps involving hypothetical performance advertised to mass audiences on public websites.

Are client testimonials allowed under the SEC Marketing Rule?

Yes, but only if the adviser satisfies the rule’s conditions.

The advertisement must clearly and prominently disclose whether the promoter is a client, whether compensation was provided, and the material terms of compensation and conflicts.

A written agreement is generally required for compensated promoters unless an exception applies, such as de minimis compensation or certain affiliate relationships.

The adviser also needs to consider whether the promoter is an ineligible person.

What is the substantiation requirement?

The substantiation requirement means that if an adviser makes a material factual claim in an advertisement, it must have a reasonable basis to believe it can substantiate that claim on demand by the SEC.

If the adviser cannot produce support, the SEC may presume the adviser did not have a reasonable basis for the claim.

This is why unsupported phrases such as “conflict-free,” “best in class,” “top adviser,” or “award-winning” can create issues if they are not properly supported and disclosed.

What have firms actually been fined for?

The largest enforcement themes include hypothetical performance on public websites, unsubstantiated or misleading claims, conflict-free statements that could not be substantiated, missing net performance alongside gross performance, inadequate recordkeeping, improperly disclosed testimonials and endorsements, and third-party ratings without required disclosures.

Penalties have ranged from tens of thousands of dollars to more than $1 million, depending on the facts.

Is this legal advice?

No.

This article is general information about how the Marketing Rule operates. Compliance depends on the specific facts, the adviser’s strategy, the audience, the communication, the disclosures, and the firm’s policies and procedures.

Confirm any marketing decision with your chief compliance officer or outside counsel before publishing.

Building a Hedge Fund Website Under the Marketing Rule

A hedge fund website does not need to be empty to be compliant.

It needs to be precise.

Strong adviser websites can still explain strategy, positioning, market focus, investor fit, process, firm history, team background, and point of view. They can still publish commentary, insights, and educational content. They can still build authority.

But the claims need to be supportable. Performance needs to be handled carefully. Testimonials, endorsements, and ratings need proper disclosures. And the entire website needs to be treated as part of the firm’s compliance and recordkeeping environment.

LeadNBFI helps financial firms build visibility and authority with compliance review in mind from the start.

If your hedge fund, private fund adviser, or financial firm is reviewing its website, content, or positioning, start with the question that matters most:

Can every material claim on this page be substantiated, balanced, disclosed, and archived?

If not, the copy is not ready.