Introduction

FINRA Rule 2210 governs communications with the public by FINRA-member broker-dealers, including investment banks and M&A advisory firms that operate through a broker-dealer registration.

The catch most marketers miss is that Rule 2210 is not just a content rule. It is an approval, supervision, filing, and recordkeeping regime that changes how a registered firm can run a website, publish thought leadership, use LinkedIn, and work with outside promoters.

For broker-dealers, marketing is not simply a question of what sounds credible. It is a question of who approved the communication, whether it needs to be filed, whether it is fair and balanced, and whether the firm can produce the records later.

This article is for general information only and is not legal advice. Rule 2210 compliance is fact-specific, and parts of the rule are subject to pending amendment. Confirm any decision with your compliance principal or outside counsel before publishing.

For Broker-Dealers, Marketing Is a Supervised Process, Not Just a Message

Most marketing advice assumes you can write something, like it, and publish it.

For a FINRA-member broker-dealer, that assumption is wrong in a way that reshapes the entire marketing function.

Under Rule 2210, a wide range of communications must be approved by an appropriately qualified registered principal before use, some retail communications must be filed with FINRA, and retail and institutional communications must be retained as records.

The content standards matter. Communications must be fair, balanced, and not misleading. But that is only part of the rule.

The part that often catches investment banks and M&A advisory firms off guard is procedural:

- Who signs off?

- When does approval happen?

- Does the communication need to be filed?

- Is the audience retail, institutional, or limited correspondence?

- Where is the record kept?

- Can the firm retrieve the communication later?

If your firm is registered as a broker-dealer, your website copy, pitch materials, LinkedIn activity, referral arrangements, and paid promotional content are not just marketing assets. They are regulated communications moving through a supervisory system.

A marketing agency that does not understand that distinction can build something that looks good and creates a compliance gap on day one.

That is why investment bank marketing and M&A advisor marketing need to be designed around the compliance workflow from the beginning.

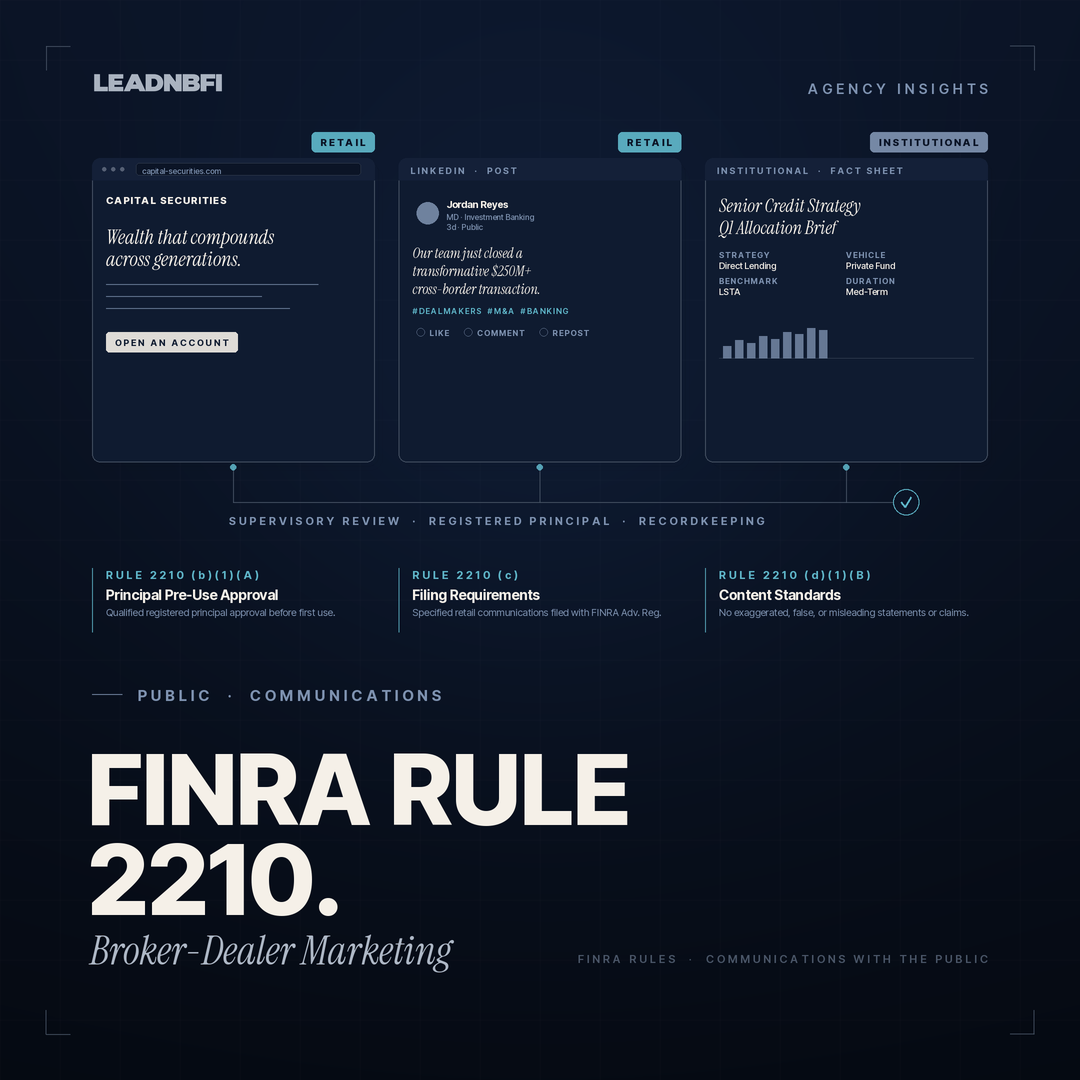

The Three Categories That Determine Everything

Rule 2210 sorts written and electronic communications into three categories.

The category determines the approval, supervision, filing, and recordkeeping obligations. The dividing line is the audience, not simply the topic or product.

Retail Communication

A retail communication is any written or electronic communication distributed or made available to more than 25 retail investors within any 30-calendar-day period.

A retail investor is any person who is not an institutional investor, whether or not that person has an account with the firm.

A public, non-password-protected website can therefore become a retail communication. So can an unrestricted LinkedIn page, a public article, a downloadable PDF, or a public campaign page.

This is the most heavily regulated category.

Correspondence

Correspondence is any written or electronic communication distributed or made available to 25 or fewer retail investors within any 30-calendar-day period.

Correspondence is subject to supervision and review, but it generally does not carry the same pre-use principal approval requirement as retail communications.

This distinction matters for one-to-one and limited-audience business development communications.

Institutional Communication

An institutional communication is a written or electronic communication distributed or made available only to institutional investors.

Institutional investor is a defined term. It includes categories such as banks, insurance companies, registered investment companies, registered investment advisers, certain employee benefit plans, FINRA members and associated persons, and certain other entities or persons that meet FINRA’s institutional definition.

This category matters enormously for investment banks and M&A advisory firms, because much of the real audience may be institutions, sponsors, qualified buyers, strategic acquirers, or sophisticated counterparties.

Institutional communications are not subject to FINRA filing and can operate under more flexible supervisory procedures than retail communications.

But there is a trap.

A firm may not treat a communication as institutional if it has reason to believe the communication, or an excerpt of it, will be forwarded or made available to a retail investor.

A gated, credential-restricted portal may support an institutional-communication framework. A public website that anyone can read generally does not.

That single architectural choice — open versus restricted — can change the regulatory treatment of the content.

The Approval and Filing Burden Most Firms Underestimate

This is what makes broker-dealer marketing different from normal business-to-business marketing.

Principal Approval

An appropriately qualified registered principal must approve each retail communication before the earlier of its use or filing with FINRA’s Advertising Regulation Department, unless an exception applies.

In plain terms: before a retail communication goes live, the required principal approval should already be documented.

Correspondence does not generally require the same pre-use principal approval, but it remains subject to supervision and review.

Institutional communications require written supervisory procedures reasonably designed to ensure compliance. If those procedures do not require principal review of every institutional communication before first use, they must include training, documentation, surveillance, and follow-up.

FINRA Filing

Filing obligations generally attach to retail communications, not correspondence or institutional communications.

Two situations matter most for a typical broker-dealer marketing program.

First, a new FINRA member must file certain retail communications used in public media, including a generally accessible website, at least 10 business days before first use for one year after FINRA membership becomes effective.

Second, specific product categories and communication types may carry their own filing requirements or timelines.

This does not mean every website update by every broker-dealer must be filed. But it does mean a broker-dealer cannot assume that public-facing marketing can be launched on a normal agency publishing schedule.

The compliance calendar and the marketing calendar have to be integrated.

Recordkeeping

Retail and institutional communications must be retained for the required period under SEC Exchange Act recordkeeping rules, and the records must include key details such as:

- A copy of the communication

- Dates of first and last use, where applicable

- The name of the approving principal and date of approval, where applicable

- The source of any statistical table, chart, graph, or illustration

- Required supporting records for performance rankings or comparisons, where applicable

Correspondence must also be retained under the applicable supervision and books-and-records requirements.

This obligation is technology-neutral. It can apply to website content, LinkedIn posts, business-related messages, videos, PDFs, pitch materials, and other communications regardless of the platform.

The practical consequence is clear: a broker-dealer cannot run marketing like a normal company.

You need a principal in the workflow, a record of approval, and an archiving system that captures the communication.

That is why corporate branding for financial firms should be built alongside compliance review and recordkeeping, not after the site is already designed.

Content Standards: Fair, Balanced, and No Projections

Rule 2210(d) sets principles-based content standards.

Communications must be based on fair dealing and good faith, must be fair and balanced, and must provide a sound basis for evaluating the facts.

They may not be false, exaggerated, unwarranted, promissory, or misleading. They also may not omit material facts if the omission would make the communication misleading in context.

Benefits must be balanced with relevant risks and limitations. Statements must be clear and not misleading for the audience receiving them.

The provision that surprises many firms coming from the adviser world is the prohibition on projections.

Rule 2210(d)(1)(F) generally prohibits communications from predicting or projecting performance, implying that past performance will recur, or making exaggerated or unwarranted forecasts.

There are narrow exceptions, including:

- Hypothetical illustrations of mathematical principles that do not predict or project investment performance

- Qualifying investment analysis tools under Rule 2214

- Price targets in certain research reports, where the price target has a reasonable basis, valuation methodology disclosure, and risk disclosure

This is meaningfully stricter than the SEC Marketing Rule that applies to investment advisers.

An investment adviser may, under specific conditions, present certain hypothetical performance. A broker-dealer generally cannot place projected annualized returns, target IRRs, or performance forecasts in broker-dealer communications unless a valid exception applies.

That gap is critical for dually registered firms.

The same business may have both adviser and broker-dealer obligations, but one clearance does not automatically solve the other. The capacity in which the firm is communicating, and the audience receiving the communication, determine which regime applies.

For private fund advisers, see our related guide to the SEC Marketing Rule for hedge fund websites.

The Projection Rule Is in Flux

One moving issue is worth tracking closely.

FINRA has proposed amendments to Rule 2210 that would permit projected performance and targeted returns in certain communications, subject to specified conditions.

As of June 12, 2026, the SEC’s SR-FINRA-2026-004 page shows the proposal still in process, with public comments due on or before June 16, 2026 and rebuttal comments due on or before June 30, 2026.

That means the existing projection prohibition should still be treated as the operative rule unless and until the amendment becomes effective.

Before relying on projected performance, target returns, or similar materials in broker-dealer marketing, confirm the current status with compliance counsel.

Testimonials Are Allowed, but Conditioned

Rule 2210(d)(6) permits testimonials in retail communications and correspondence, but only with conditions.

If a testimonial concerns a technical aspect of investing, the person giving it must have the knowledge and experience to form a valid opinion.

If the testimonial concerns the investment advice or investment performance of a member or its products, the communication must prominently disclose:

- That the testimonial may not be representative of the experience of other customers

- That the testimonial is no guarantee of future performance or success

- If more than $100 in value was paid for the testimonial, that it is a paid testimonial

For dually registered firms, the SEC Marketing Rule’s separate testimonial and endorsement conditions may also apply.

The two regimes are not identical.

A testimonial that seems acceptable under one framework may still create issues under the other, depending on the firm’s registration, the capacity in which it is communicating, the audience, the compensation arrangement, and the distribution channel.

This is exactly the kind of overlap where firms assume one review covers everything and then discover a gap during an examination.

Websites and Social Media: Open Pages, Interactive Posts, and Third-Party Content

FINRA’s digital guidance applies Rule 2210 to websites and social media through a practical distinction between static content, interactive content, and third-party content.

Public Static Content

A public website page, public LinkedIn profile, social media profile background, pinned post, or downloadable public PDF may be treated as a retail communication when it is available to more than 25 retail investors within a 30-day period.

That means public-facing content needs to be reviewed through the retail-communication lens before it goes live.

This matters for LinkedIn marketing for financial firms, where the line between professional visibility and regulated communication can be easy to underestimate.

Interactive Content

Retail communications posted on an online interactive electronic forum are excepted from the prior-to-use principal approval requirement if they are supervised and reviewed in the same manner as correspondence.

That does not mean interactive posts are unregulated.

They still need supervision, content controls, training, and recordkeeping. And if interactive content is later copied into static form, it can become subject to the advertising approval rules again.

Third-Party Content and Links

Unsolicited third-party comments are generally not treated as the firm’s own communications.

But two concepts change the analysis: entanglement and adoption.

If the firm paid for, helped prepare, influenced, or arranged the content, FINRA may treat the firm as entangled with it.

If the firm explicitly or implicitly endorses third-party content — for example by sharing, liking, or otherwise approving it — FINRA may treat the firm as having adopted it.

Once entanglement or adoption applies, the content can become the firm’s communication and may be subject to the full content, approval, supervision, and recordkeeping framework.

The same logic applies to links. A firm cannot link to third-party content it knows, or has reason to know, is false or misleading. Depending on how a link is used, the firm may also be treated as adopting the linked content.

Where Firms Actually Get Fined: Influencers

The clearest recent enforcement signal is FINRA’s focus on social media influencers.

In March 2024, FINRA fined M1 Finance $850,000 in its first formal enforcement action involving a firm’s supervision of social media influencers.

Between January 2020 and April 2023, M1 paid influencers to promote the firm and instructed them to include unique links that prospective customers could use to open and fund M1 brokerage accounts.

FINRA found that the influencer posts were not fair or balanced, or contained exaggerated, unwarranted, promissory, or misleading claims.

Because the posts were made on the firm’s behalf, they were treated as retail communications subject to Rule 2210.

FINRA also found that M1 did not review or approve the influencer posts before use, did not retain those communications, and did not have a reasonable supervisory system for them.

The lesson for broker-dealers, investment banks, and M&A advisory firms is direct.

The moment you compensate someone to promote the firm, that content may become your advertisement.

It needs the right approval process, the right disclosures, the right content standards, and the right records.

Referral partners, paid promoters, influencer arrangements, podcast sponsorships, and third-party content programs should not sit outside the marketing-compliance perimeter. For a broker-dealer, they are often inside it.

How Compliant Broker-Dealers Market Effectively

None of this prevents a broker-dealer from building a strong, credible marketing presence.

It changes how the system has to be built.

The firms that do it well usually share a few practices.

They Build the Approval Workflow Into Marketing From the Start

Principal approval, supervision, and recordkeeping should be part of the publishing pipeline, not an afterthought.

The website, CMS, review process, and archive should be designed together.

A broker-dealer marketing program should be able to answer a simple question at any time:

Who approved this communication, when, and on what basis?

They Use the Institutional-Communication Category Deliberately

Where the real audience is institutions, sponsors, qualified buyers, strategic acquirers, and professional counterparties, a gated, credential-restricted environment may allow deeper and more specific communication than a public retail page.

That does not remove the need for supervision or records. But it can align the content environment with the intended audience.

For public pages, keep the content disciplined. For richer, audience-specific materials, use architecture that reflects the regulatory category.

They Build Authority Through Judgment, Not Forecasts

Because broker-dealers face strict limits on projections, differentiation often has to come from visible judgment rather than forecasted returns.

Sector insight, transaction perspective, process clarity, market commentary, and an articulate point of view can build trust without stepping into prohibited projection language.

That is where content marketing for financial services becomes valuable. It lets a firm demonstrate expertise without relying on exaggerated claims, unsupported superiority language, or performance forecasts.

They Keep the Public Website Disciplined

A broker-dealer website can still be strong.

It can explain the firm’s focus, sector expertise, services, team, transaction process, buyer psychology, and point of view.

But public-facing copy should avoid:

- Projected returns

- Target IRRs

- Promissory language

- Unsupported superiority claims

- Misleading comparisons

- Implied guarantees

- One-sided benefit statements without risk or limitation context

- Unapproved testimonials or paid endorsements

Good SEO and GEO for financial services does not require hype. It requires clarity, structure, specificity, and credible substance.

They Treat Compensated Relationships as Advertising Risk

If someone is paid to promote the firm, the firm should assume the content needs review.

That includes influencers, referral partners, paid newsletter placements, podcast sponsorships, content affiliates, and other promotional relationships.

The content may need to be clearly identified as advertising, approved before use, supervised, retained, and supported by required disclosures.

For broker-dealers, outsourcing promotion does not outsource responsibility.

The Core Lesson

FINRA Rule 2210 does not make broker-dealer marketing impossible.

It makes process inseparable from message.

For investment banks and M&A advisory firms, the goal is not to avoid marketing. The goal is to build a marketing system that understands the category, the audience, the approval process, and the recordkeeping obligation before anything goes live.

The firms that get into trouble usually let marketing outrun supervision.

The firms that build durable visibility do the opposite.

They make the compliance architecture and the marketing architecture part of the same project.

That is how regulated financial firms can become more visible without becoming careless.

Frequently Asked Questions

Does FINRA Rule 2210 apply to investment banks and M&A advisory firms?

It applies to FINRA-member broker-dealers.

Investment banks and M&A advisory firms that operate through a broker-dealer registration are subject to Rule 2210 for communications with the public, including websites, marketing materials, LinkedIn content, and certain promotional programs.

A firm that is not a broker-dealer may be governed by different rules.

Does a broker-dealer website need approval before it goes live?

Generally, public static website content should be reviewed through the retail-communication framework when it is available to more than 25 retail investors within a 30-day period.

Retail communications generally require approval by an appropriately qualified registered principal before the earlier of use or filing with FINRA, unless an exception applies.

New FINRA members may also have pre-use filing obligations for certain public-media retail communications, including generally accessible websites, for the first year of membership.

What is the difference between retail, correspondence, and institutional communications?

The categories are defined by audience.

Retail communications reach more than 25 retail investors in a 30-day period and carry the heaviest requirements.

Correspondence reaches 25 or fewer retail investors and is supervised and reviewed, but generally does not require the same pre-use principal approval as retail communications.

Institutional communications are distributed only to institutional investors and are not filed with FINRA, but they still require written supervisory procedures and records.

Can a broker-dealer show projected performance or target returns in marketing?

Generally no, unless a valid exception applies.

Rule 2210(d)(1)(F) generally prohibits communications from predicting or projecting performance, implying that past performance will recur, or making exaggerated or unwarranted forecasts.

FINRA has proposed amendments that would allow projected performance and targeted returns in certain communications under specified conditions, but as of June 12, 2026, the SEC process for SR-FINRA-2026-004 is still pending.

Confirm the current status before relying on projections in broker-dealer marketing.

How does Rule 2210 treat social media influencers?

If a broker-dealer arranges for, pays for, or is involved in preparing an influencer post, FINRA may treat the firm as entangled with the communication.

That can make the influencer post the firm’s own retail communication.

The content then needs to meet Rule 2210 standards, follow the required approval and supervisory process, include any required disclosures, and be retained as a record.

What records does a broker-dealer need to keep for marketing?

Retail and institutional communications must generally be retained under the applicable Exchange Act and FINRA books-and-records requirements.

Records should include a copy of the communication, dates of use, the approving principal and approval date where applicable, and the source of any statistics, charts, graphs, or illustrations.

Correspondence is also subject to applicable supervision and recordkeeping requirements.

How does Rule 2210 differ from the SEC Marketing Rule?

Rule 2210 governs FINRA-member broker-dealers. The SEC Marketing Rule governs investment advisers registered or required to register with the SEC.

Rule 2210 adds a category-based approval, supervision, filing, and recordkeeping system and includes a stricter general prohibition on projections.

A dually registered firm must apply the correct regime to each communication based on the capacity in which it is acting and the audience receiving the communication.

The two rule sets are related, but they are not interchangeable.

Is this legal advice?

No.

This article is general information about how Rule 2210 operates. Obligations depend on the firm’s registration, communication type, audience, products, distribution method, supervisory procedures, and current regulatory status.

Confirm any marketing decision with your compliance principal or outside counsel before publishing.

Building Broker-Dealer Marketing Under Rule 2210

Broker-dealer marketing does not have to be weak.

It has to be controlled.

A strong broker-dealer website can explain the firm’s advisory focus, sector specialization, transaction perspective, team credibility, and point of view. A strong LinkedIn presence can make senior professionals more visible. A strong content program can build trust before the first conversation.

But the publishing system must reflect the rule.

Before content goes live, the firm should know:

- Which communication category applies

- Whether principal approval is required

- Whether FINRA filing is required

- What records must be retained

- Whether any testimonial, endorsement, projection, comparison, or third-party content issue is present

- Whether the communication is fair, balanced, and not misleading

LeadNBFI helps financial firms build visibility and authority with compliance review in mind from the start.

If your broker-dealer, investment bank, or M&A advisory firm is reviewing its website, LinkedIn presence, content program, or brand positioning, start with the operational question that matters most:

Can this communication be approved, filed if required, substantiated, supervised, and archived?

If not, the marketing system is not ready.

Contact LeadNBFI to discuss a compliance-aware visibility strategy for your financial firm.